|

Check out this article about a FL CCRC with a $1.5-million+ entrance fee! Then read our exclusive report on creating your own "Private CCRC Plan". A Comfort LTC Exclusive:How & why to create a "Private CCRC Plan"

0 Comments

Hybrid (or "linked-benefit", "combo" or "asset-based") LTC insurance options are exploding in the marketplace, and they are NOT all created equal. Are "hybrid" LTC policies with a death benefit really a better deal? You'll be surprised at what our analysis shows, and why you need to make sure you know ALL your options before you buy LTC insurance.

The new Comfort LTC Hybrid LTCI Information Center will provide clear explanations of the many different types of plans along with detailed case study analysis to provide real-world examples and comparisons. CLICK HERE

|

Age at end of 2020 |

Maximum Deductible Premium |

40 or less |

$ 430 |

41 to 50 |

$ 810 |

51 to 60 |

$ 1,630 |

61 to 70 |

$ 4,350 |

71 and older |

$ 5,430 |

HOWEVER, if you have funds in a Health Savings Account (HSA) - or an employer-funded Health Reimbursement Account (HRA) - you CAN use those tax-free dollars to pay tax-qualified LTC insurance premiums up to the age-based, Eligible Premium amount shown above.

BUSINESS OWNERS (and spouses) get to take the age-based, Eligible Premium deduction "above-the-line" on page one of Form 1040 as part of the "Self Employed Health Insurance Deduction" (Line 29). This applies to owners of business incorporated or taxes as: Sole Proprietorships, Partnerships, or S-Corporations. (Shareholder/Employees of a "regular" C-Corporation can have the entire premium deducted - without limit - if paid as an employee benefit by the corporation.)

CLICK HERE TO LEARN MORE ABOUT BUSINESS DEDUCTIONS FOR LTCI.

The plan will provide $100 per day of benefits which will increase with inflation for a maximum of 365 days (1-year). Each day of benefits is considered a "unit" of coverage and units can be combined to pay for care services above $100/day, but that would also shorten the total benefit period. The benefit can be used to pay family members to provide care after they have completed a minimum amount of mandatory training.

Every employee in the state will have a payroll tax withholding to pay for the plan. The tax is 0.58%, or $0.58 for every $100 in payroll income. A person earning $4,000 per month would pay $23.20 per month.

Payroll deductions will not begin for 3 years, and no benefits will be paid for at least 3 years after that as the plan requires that employees pay in for a minimum of 3 of the previous 6 years to be eligible. To be fully "vested" in the plan an employee must pay in for at least 10 years.

"Self employed" people will not be automatically covered, but can opt-into the plan at the same payroll tax rate.

Employees who have private LTC insurance can opt-out of the tax and coverage.

A TV station in Houston, KHOU, even found an internet post from 2004 with nearly the same wording as this old-is-new-again misleading social media joke.

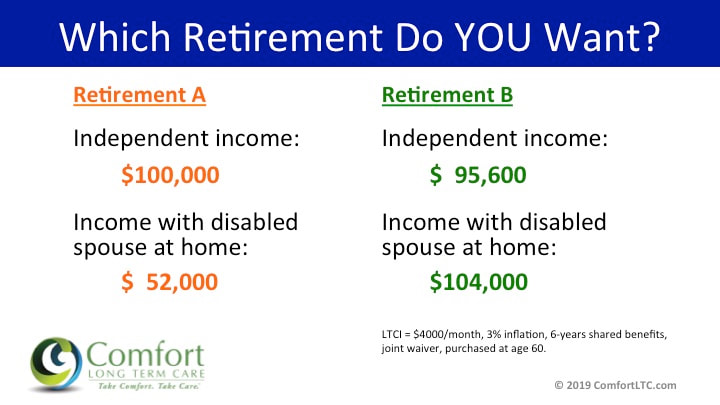

You can't compare "independent retirement living" with CARE in a nursing home - or an assisted living facility. Hotel staff - nor cruise ship staff - will bathe and dress you, help you to and from the toilet, nor will they make sure your dementia doesn't lead you out the front door into traffic - or over the rail into the ocean - in the middle of the night. Once you need CARE, you'll be on the curb - or the dock.

CLICK HERE to read my 2016 blog post for more details on why this is a ridiculous idea.

Licensed agents and advisors can access the new NAIFA Center for Limited and Extended Care Funding at: https://naifa.lifehappenspro.org

Click "Read More" below to check out this great infographic, and let us know if we can help you with any of your Medicare questions!

for older posts

Author

Bill Comfort

CSA, CLTC, LTCCP

The LTCpro®

Categories

All

Alzheimer's

Caregiving

Commentary

LTC Insurance

LTC Planning

LTC Tax Planning

Medicare

News

Rate Increases

Video

Archives

November 2023

October 2022

December 2021

February 2021

December 2020

October 2020

August 2020

June 2020

May 2020

April 2020

March 2020

January 2020

November 2019

September 2019

May 2019

March 2019

February 2019

October 2018

August 2018

March 2018

January 2018

August 2017

July 2017

March 2017

February 2017

November 2016

October 2016

August 2016

July 2016

June 2016

May 2016

April 2016

January 2016

November 2015

October 2015

August 2015

May 2015

April 2015

March 2015

February 2015

January 2015

December 2014

November 2014

RSS Feed

RSS Feed